Reciprocal (algebraic) method of cost allocation

The allocation of service department costs is incomplete if the method used for cost allocation ignores or does not give full recognition to interdepartmental services. Interdepartmental services are services that two or more service departments provide to each other. For example, consider a case where service department A provides service to service department B, and in turn, department B provides service to department A.

If you have already studied direct method and step method of cost allocation you may have noticed that the direct method completely ignores the interdepartmental services and step method gives them only a partial recognition because it allocates costs forward – never backward. To overcome this problem, a method known as reciprocal method is used which fully recognizes interdepartmental services and provides greater exactness in allocating the cost of a service departments to other departments. The reciprocal method uses the simultaneous equations technique and is therefore also referred to as simultaneous equations method and algebraic method of departmental cost allocation.

Example

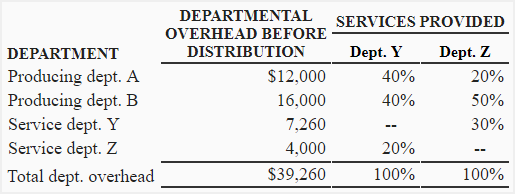

A company has two service departments and two producing departments. The two service departments provide service not only to two producing departments but also one another. The costs of four departments and relationship among them is shown below:

Required: Allocate the cost of service departments to producing departments using reciprocal/algebraic method.

Solution

Let:

Y = $7,260 + 0.3Z —— Eq.1

Z = $4,000 + 0.2Y —— Eq.2

Substituting the value of Z in equation 1:

Y = $7,260 + 0.3($4,000 + 0.2Y)

Y = $7,260 + $1,200 + 0.06Y

Y – 0.06Y = $7,260 + $1,200

0.94Y = $8,460

Y = $8,460/0.94

Y = $9,000

Substituting the value of Y in equation 2:

Z = $4,000 + 0.2(9,000)

Z = $4,000 + $1,800

Z = $5,800

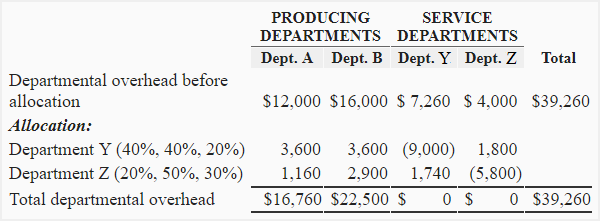

Distribution summary:

Advantages and disadvantages of reciprocal or algebraic method

The major advantage of reciprocal or algebraic method is that it fully takes into account the interdepartmental services. It is therefore considered a more accurate method than direct and step method for departmental cost allocation.

The major disadvantage of reciprocal method is that it is more complex when compared with direct and step method. The use of a computer software could solve the complexity issue involved in this method but there is no sufficient evidence that this solution has significantly increased the popularity of reciprocal method. Moreover, the step method produces results that are usually close to the results produced by complex reciprocal or algebraic method.

I am happy for the explanation thank more lwill see..next

The work on advantage and disadvantage in good but too brief