Par value stock

Definition and explanation

Par value stock is a type of common or preferred stock having a nominal amount (known as par value) attached to each of its shares. Par value is the per share legal capital of the company that is usually printed on the face of the stock certificate. It is also known as the stated value and face value of stock.

Companies are free to choose any amount as the par value for their share, but they mostly choose a very low amount for their common stock. For example, the common stock of Microsoft has a par value of $0.00000625 per share, and Ford’s common stock has a par value of $0.01 per share.

Presentation of par value stock in balance sheet

A company must report the par value of its total subscribed and outstanding shares in its annual financial statements. For example, if a stock’s par value is $0.50 per share and the issuing company has 100,000 shares of common stock outstanding at the end of its reporting period, then the common stock in the amount of $50,000 (= $0.50 x 100,000 shares) would be recorded as a line item of stockholders’ equity. The proper presentation of both par value common stock and par value preferred stock can be made as follows:

Par value vs market value of stock

The par value of a stock is different from its market value. In common stock trading, par value usually plays a negligible part. Companies set a par value for their common stock because they are often legally required to do so. In the case of common stock, it just represents a legally binding contract that the stock will not be sold below a certain price, like $0.1 per share or $0.01 per share, etc. Moreover, the par value of a common stock often doesn’t have any connection with its dividend rate. Rather, the dividends on common stock are generally announced as a certain dollar amount per share, like $5 per share or $10 per share, etc. To determine the dividend yield metric, investors can simply divide this per share dividend amount by the per share cost.

Once set, the par value of stock remains fixed forever unless the issuing company executes a forward or reverse stock split to increase or decrease the number of its outstanding shares.

The role of par value in relation to a preferred stock is more important than the common stock in that the annual dividend associated with this class of equity is listed as a percentage of its par value. This percentage linked to the preferred stock is often referred to as its coupon rate. For instance, a share of preferred stock with a $1,000 par value and a 15% coupon rate would generate a $150 (= $1,000 x 15%) annual dividend for its holder. Similarly, a share of 10% preferred stock with a $50 par value would earn a $5 (= $50 x 10%) dividend for investors.

The market price per share, on the other hand, refers to the per share value or worth at which a company’s stock is actually traded in the secondary market. Unlike par value, a stock’s market price is generally subject to frequent fluctuations and is largely determined by investors’ perceptions of the future of the stock and the operations of its issuing company.

The market price of the stocks of successful and well established companies is usually found to be much higher than their par value. For example, at the time of writing this article, the par value of Amazon’s stock is $0.01 per share, and its market value is $3,580.41 per share, which is 358,041 times higher than the par value. Similarly, the par value of Apple’s stock is $0.00001, but today it is being traded at $161.94 per share.

[Sources: https://finance.yahoo.com/lookup/; November 24, 2021 4:00PM EST]

Journal entries for the issuance of par value stock

The par value stock can be issued in three ways: at par, above par, and below par. A brief explanation and journal entries for all the situations are given below:

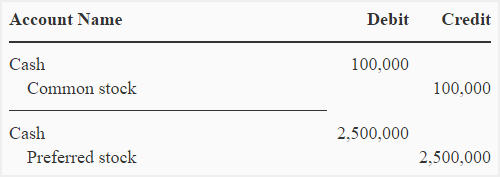

(1) At par:

When stock is issued at a price equal to its par value, it is said to be issued at par. The journal entry is given below:

(i). When common stock is issued at par:

(ii). When preferred stock is issued at par:

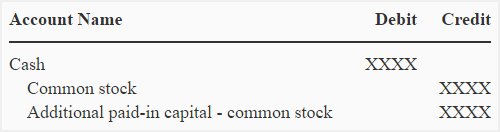

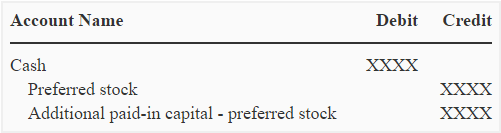

(2) Above par:

When stock is issued at a price higher than its par value, it is said to have been issued above par. When stock is issued above par, the cash account is debited with the total amount of cash received, the capital stock account is credited with the total par value of shares issued, and an account known as “additional paid-in capital” or “capital in excess of par” is credited with the difference between cash received and the par value of shares issued. This can be summarized in the form of the following journal entry:

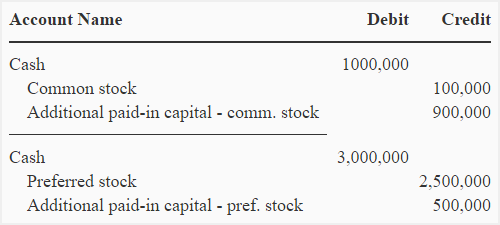

(i). When common stock is issued above par:

(ii). When preferred stock is issued above par:

The additional paid-in capital is a part of total paid up capital that increases the stockholders’ equity.

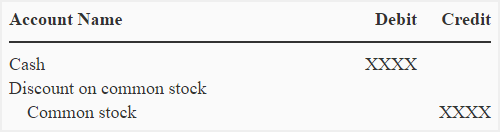

(3) Below par:

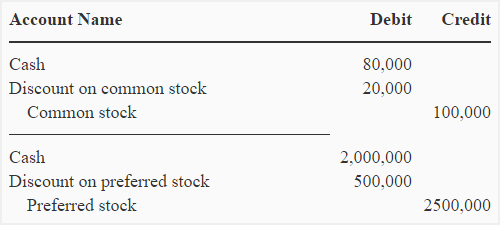

When stock is issued at a price lower than its par value, it is said to have been issued below par. In such an issue, the cash account is debited with the total amount of cash received, the discount on the issue of capital stock account is debited with the difference between the amount received and the par value of shares issued, and the common stock account is credited with the par value of the shares issued. The journal entry for such an issue is given below:

(i). When common stock is issued below par:

(ii). When preferred stock is issued below par:

The discount on stock reduces stockholders’ equity.

In practice, the issuance of stock at a discount (i.e., below its par value) is not usual because it is legally prohibited in many countries and states. This legal restriction partially explains why companies mostly choose a very low par value for their stock.

Example

The Northern Company issued 100,000 shares of its $1 par value common stock and 25,000 shares of its $100 par value preferred stock. Make journal entries to record these transactions in the books of Northern Company if the shares are issued:

- at par.

- at $10 per share of common stock and $120 per share of preferred stock.

- at $0.8 per share of common stock and $80 per share of preferred stock.

Solution:

(i). When common and preferred shares are issued at par:

(ii). When common and preferred shares are issued above par:

(iii). When common and preferred shares are issued below par:

Notice that in all the cases discussed above, both common and preferred stocks have been recorded at their par value. When a company receives more than the par value, it records a credit in the “additional paid-in capital common/preferred stock account,” and when, on the other hand, it receives less than the par value, it records a debit in the “discount on common/preferred stock account.”

Impact on statement of cash flows

The sale of equity is one of the major financing activities for a business entity, and any cash that this activity brings into the business is categorized as such while drafting a statement of cash flows. The line items used for its reporting in the statement of cash flows are “issuance of common stock,” if the common shares are sold, and “issuance of preferred stock,” if the preferred shares are sold. Learn more about financing cash flows here.

Very nice, thank you very much.